Corporate income tax rates

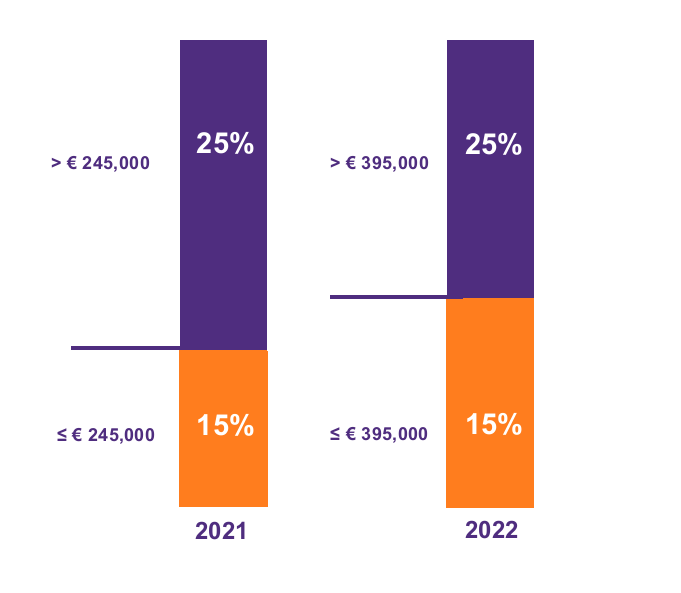

Currently, Dutch corporate income tax is levied through two profit brackets. In 2021, the first profit bracket applies to profits up to and including € 245,000 which are subject to a corporate income tax rate of 15%. All profits in excess of this amount are subject to a corporate income tax rate of 25%. According to previously announced plans, the profit threshold of the first corporate income tax bracket will be increased from € 245,000 to € 395,000 in 2022. Contrary, to some expectations, this reduction will go ahead in 2022.

![Tax Plan 2022 - Corporate income tax rates.png]()

Environmental investment allowance (MIA)

Dutch tax law includes an investment deduction for certain investments in environmentally friendly business assets. The government has decided to raise the deduction percentages. The previous rates were 13,5%, 27% and 36%. As of 1 January 2022, the rates will be raised to 27%, 36% and 45%.

Transfer pricing corrections

In the Netherlands, transactions between group entities should reflect a fair market value, i.e., need to be at arm`s length. In case a transaction is not in accordance with the arm`s length principle, a downwards or an upwards transfer pricing adjustment takes place at the level of the Dutch corporate income tax payer via an informal capital contribution or a deemed dividend distribution. However, in case the country of the related counterparty does not recognize such a transfer pricing adjustment, an international mismatch may occur which could result in e.g. a deduction without a pick up.

The legislative proposal specifies that as of 1 January 2022, the taxable profit of a Dutch taxpayer can no longer be adjusted downwards if the taxable profit of the other group company is not adjusted upwards accordingly. The legislative proposal also provides for a rule regarding the onshoring of assets from a group company to the Netherlands. In case the transferring company is not obliged to adjust the sales price of these assets to a fair market value, the Netherlands will refuse to provide a step-up to the fair market value of the assets at the acquiring company.

Reversed hybrid mismatches

Per 2020, the anti-hybrid mismatch rules of ATAD2 apply in the Netherlands with the exception of reversed hybrid mismatch rules. This rule will become effective as per 1 January 2022. A reverse hybrid entity is an entity (generally a partnership) that for tax purposes is considered transparent in its jurisdiction of incorporation/establishment, whereas the jurisdiction of one or more related participants qualifies the entity as non-transparent. In short, the reverse-hybrid measure aims to tackle the hybrid mismatch at the source by making the hybrid entity subject to tax. Effectively, a reverse hybrid entity will become subject to Dutch corporate income tax only to the extent that the profit is attributable to related participants that qualify the entity as non-transparent. Similarly, distributions by a reverse hybrid entity will only become subject to withholding tax to the extent the distribution is attributable to related participants that qualify the entity as non-transparent.

CFC-rules

Under the CFC-rules certain types of income derived by low-taxed foreign subsidiaries or permanent establishments are subject to corporate income tax at the level of the Dutch parent company. In case any profit tax is levied at the level of the CFC, these taxes can under conditions be credited with the Dutch corporate income tax which is levied at the level of the Dutch parent company.

However, the compensation of foreign profit taxes is maximized up to the Dutch corporate income tax payable in a financial year. Foreign profit taxes - which cannot be compensated as a result of this limitation – can be taken into account in the next financial year. The foreign profit tax which can be credited must be determined per CFC.

Currently, the Dutch corporate income tax act does not specify in which order the compensation of foreign profit taxes must take place. On Budget Day 2021, it is announced that the foreign profit taxes must be credited in order starting from the smallest amount.

Settlement of withholding tax with corporate income tax

The government plans to limit the settlement of dividend withholding tax and games of chance tax with corporate income tax. The cause of this limitation is a decision by the EU Court of Justice on 22 November 2018 (Sofina-ruling )

A Dutch receiving corporate shareholder can offset the dividend withholding tax (and games of chance tax) against its corporate income tax. In case the Dutch corporate shareholder is in a loss-making position for corporate income tax purposes, it can claim a full refund of the dividend withholding tax (and games of chance tax). This reclaim option is not available to foreign corporate shareholders. According to the EU Court of Justice this incompatible with EU law.

The government therefore has announced that the refund system will be replaced by a carry-forward of paid withholding taxes. Starting from 2022, the withholding taxes can only be offset against corporate income tax due in that financial year. The remaining withholding taxes can be carried forward indefinitely.

Other points for 2022

Loss compensation

Currently, all tax losses can be carried back for one year and can be carried forward for a period of six years. The government’s plan specifies that starting from 2022, tax losses can be carried forward indefinitely. However, the amount of losses which can be set-off will be limited. Profits up to € 1 million can be fully used to offset losses. In case the taxable profit exceeds €1 million, only 50% of the remaining taxable profit may be used to set-off losses. The losses which cannot be set-off may be carried forward indefinitely to the following years. The measure has been confirmed to apply from 1 January 2022.

Qualification of (foreign) partnerships

Earlier this year, the government announced that it will change the Dutch qualification rules for foreign partnerships. The aim of this change is to combat tax avoidance as a result of qualification mismatches. As a result of these changes, certain types of partnerships would be qualified differently than before. The government decided not to include this proposal in the Tax Plan 2022. As a result, the envisaged measure will not enter into force per 1 January 2022.