CBAM

Carbon Border Adjustment Mechanism (CBAM)

Everything you need to know about the levy on CO2 emissions from imported goods from outside Europe.

In order to address the tax issues that arise from the increasing digitalization of economies, the OECD has been working on a Two-Pillar solution that reforms the current international taxation rules. The first (“Pillar 1”) seeks to shift tax on large digital service providers into the countries in which their sales take place. The second (“Pillar 2”) seeks to establish a minimum global tax rate.

At a very high level, Pillar 1 is intended to reallocate profits and related taxing rights from certain jurisdictions where multinational enterprises (MNEs) have physical substance to other countries where they have a market presence, regardless of whether or not they have a physical presence in that second jurisdiction.

Pillar one will apply to multinational enterprises with a global turnover above 20 billion euros and a profitability above 10% (i.e. profit before taxes). It is envisaged that this will operate as some type of digital sales/services tax (“DST”), with global technology giants falling within the rules.

Sectors of the extractive industry and regulated financial services are excluded from the scope.

After 7 years there will be a review to verify whether the new system was successfully implemented and achieved tax certainty. If so the global turnover minimum will be decreased to 10 billion euros.

In order to determine the profit allocation to market jurisdictions, Pillar One uses two different formulas called:

Amount A allocates a share of the residual profits of a MNE to jurisdictions where the MNE has sales. This allocation is based on a formula, not the arm’s length principle.

The new taxing right would apply to 25% of the profit exceeding 10% of revenue (Amount A).

Amount A would be apportioned pursuant to a revenue-based allocation key between jurisdictions where the MNE realises at least EUR 1 million of revenue (for jurisdictions with a GDP below EUR 40 billion, a lower threshold of EUR 250,000 would apply).

Amount B provides a fixed return on certain basic marketing and distribution activities that take place in a certain jurisdiction.

Amount A will be implemented through a multilateral instrument scheduled to be signed as of 2022 with entry into force in 2023. Unilateral measures, including digital services taxes, shall be removed.

The work on Amount B continues to be postponed to end of 2022. Moreover, no details on the specifics of Amount B or of its scope have been published.

Broadly, Pillar 2 is the global anti-base-erosion (“GLOBE”) regime which proposes to implement an agreed minimum effective tax rate of 15% in each country in which a MNE operates. The idea is that Pillar Two will end the race to the bottom.

The GloBE rules apply to multinational enterprises with a consolidated group revenue of at least EUR 750 million. However, countries are free to apply the IIR to MNE’s headquartered in their country even if they do not meet the threshold.

Furthermore, under certain circumstances a number of organizations will be exempt and are therefore not subject to the GloBE rules, such as investments funds, pension funds and real estate investment vehicles.

Pillar Two consists of the following key rules:

GloBE consists of two connecting domestic rules:

The GloBE rules will provide for an exclusion from the UTPR (under taxed payment rule) for MNE’s in the initial phase of their international activity. MNE’s in the initial phase are defined as:

This exemption is limited to a period of 5 years starting from the moment the MNE’s fall into the scope of the GloBE rules. As such, MNE’s that fall into the scope at the time the GloBE rules come into effect will be subject to the UTPR 5 years from the time the UTPR comes into effect.

The GloBE rules will contain a de minimis exclusion rule and a formulaic substance carve-out rule.

The de minimis rule excludes those jurisdictions where the MNE has revenues of less than EUR 10 million and profits of less than EUR 1 million.

The formulaic substance carve-out rule will exclude an amount of revenues representing the substance the MNE has in a jurisdiction.

The STTR will act as a withholding tax levy and will block treaty benefits when the payment is subject to a tax rate below the minimum rate of 9% at the level of the recipient. The STTR is meant to combat certain payments that present a high risk of profit shifting to low-tax jurisdictions. As such, the STTR applies to interest, royalties, and a defined set of other payments. The rule would apply to aforementioned payments made from a developing country to IF member States that apply a nominal corporate income tax rate below the STTR minimum rate of 9% to these payments. Moreover, the STTR shall take priority over the other rules.

In certain situations the IIR may be blocked by tax treaties. Therefore Pillar Two includes a switch-over rule to remove treaty blockades. If for example a tax treaty stipulates the parent jurisdiction to exempt the income of a permanent establishment that is established in a low-taxing State, the Switch-Over Rule allows for a switch from the exemption method to the credit method.

Pillar two should be implemented in 2022 and is envisioned to take effect per 2023. The UTPR is scheduled to come into effect in 2024.

Hereafter we will discuss the above mentioned rules in depth with a few examples.

The ETR in State B amounts to 12% which is below the minimum of 15%. Therefore, the taxes levied under the IIR: EUR 30 (Sub1 GloBE tax base: 1,000 * 3%).

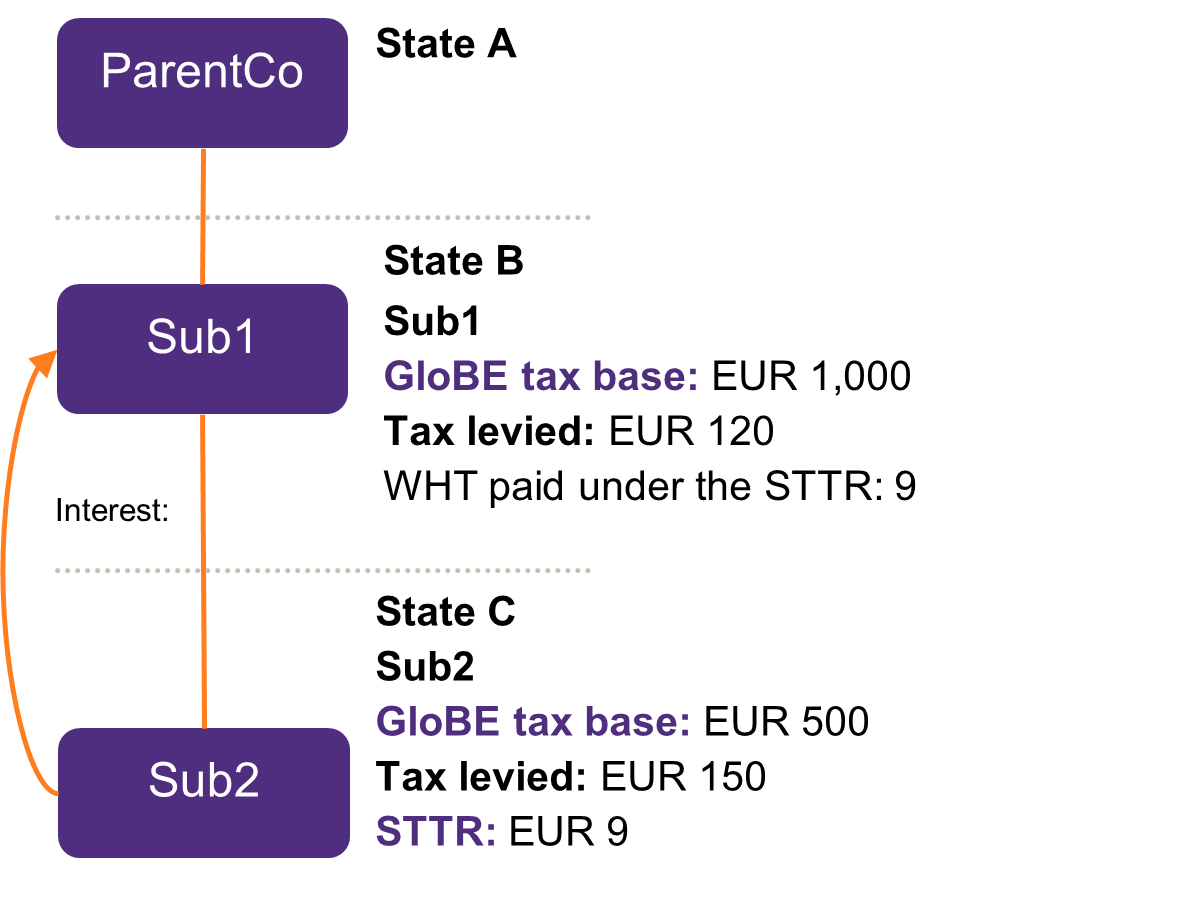

In this example we focus on State B and State C. In this case State B exempts any offshore income and State C qualifies as a developing country. Therefore, State C is authorized to impose additional tax on the interest at the rate equal to the difference between the corporate income tax levied with respect to the interest payment at the level of the recipient (0%) and the minimum rate under the STTR (9%).

Taxes under the STTR: EUR 9 (100*9%).

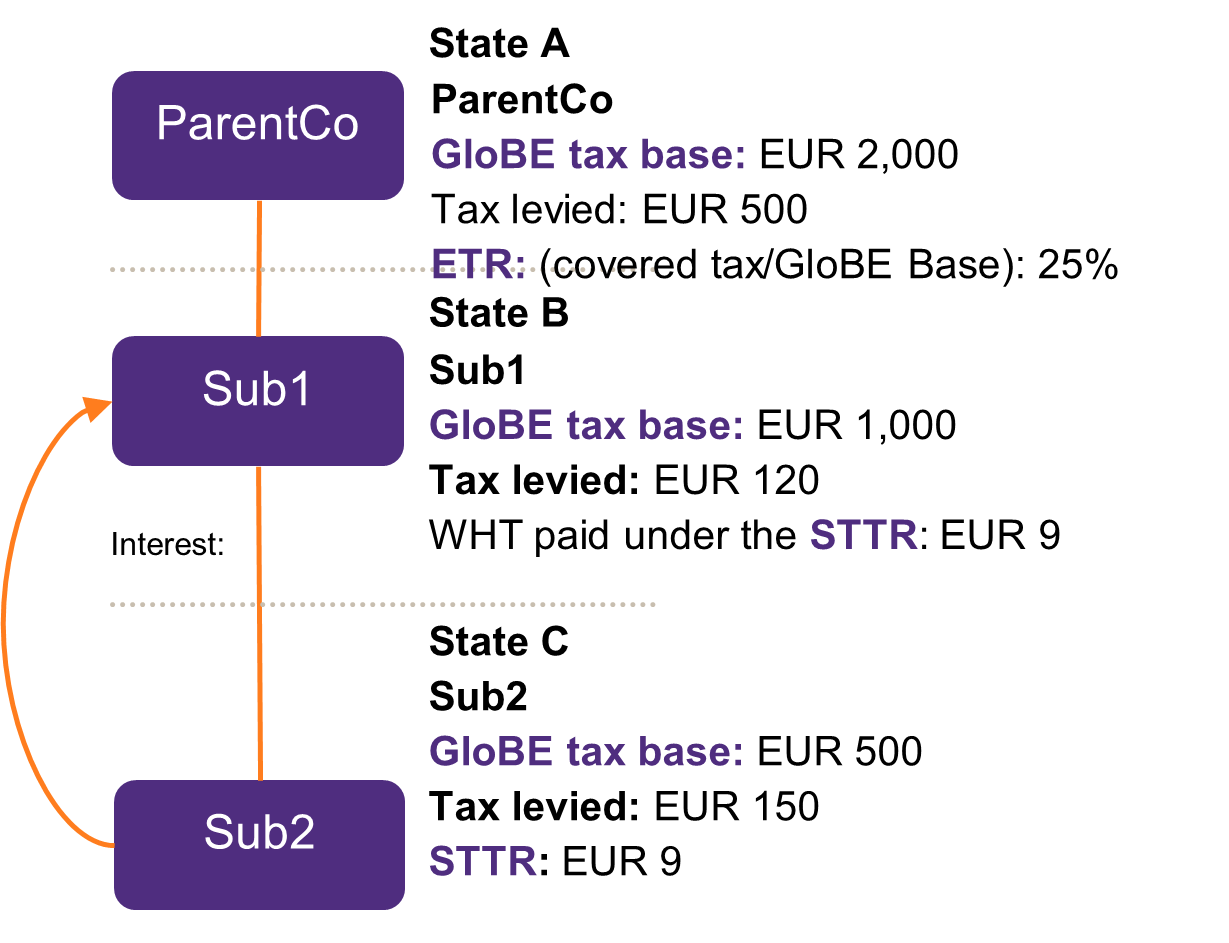

In this case State A has not introduced the IIR. State C qualifies as a developing country and has implemented the UTPR. State B exempts any offshore income.

Taxes under the STTR: EUR 9 (100*9%)

Therefore the ETR in State B amounts to 12.9%.

Taxes levied under the UTPR should amount to EUR 21 (Sub1 GloBE tax base: 1,000 * 2,1%) As such State C will deny the deduction of the interest under the UTPR up to: EUR 70 (21 / 30%).

The political pressure to come to an agreement by 2023 is high, however a significant amount of technical work as well as political work still remains. Therefore, implementing Pillar One and Two by 2023 seems to be ambitious.

Pillar One and Two aim to drastically change to landscape of international taxation and increase the complexity of the international tax system. This could have far reaching consequences for MNE’s that fall within the scope of Pillar One and Two.

We recommend to gather relevant information such as the effective tax rates per jurisdiction and make an assessment how Pillar One and Two have an impact on your business. Subsequently we recommend to make an impact assessment which could lead to rethinking the current structure.

Of course we can assist you with the obligations arising from Pillar One and Two. We can help you with the assessment of the precise impact that Pillar One and two will have on your company as well as assist you with your compliance framework. We will keep you informed on any further developments and can help you in the complete process. Please contact us if you have any further questions.