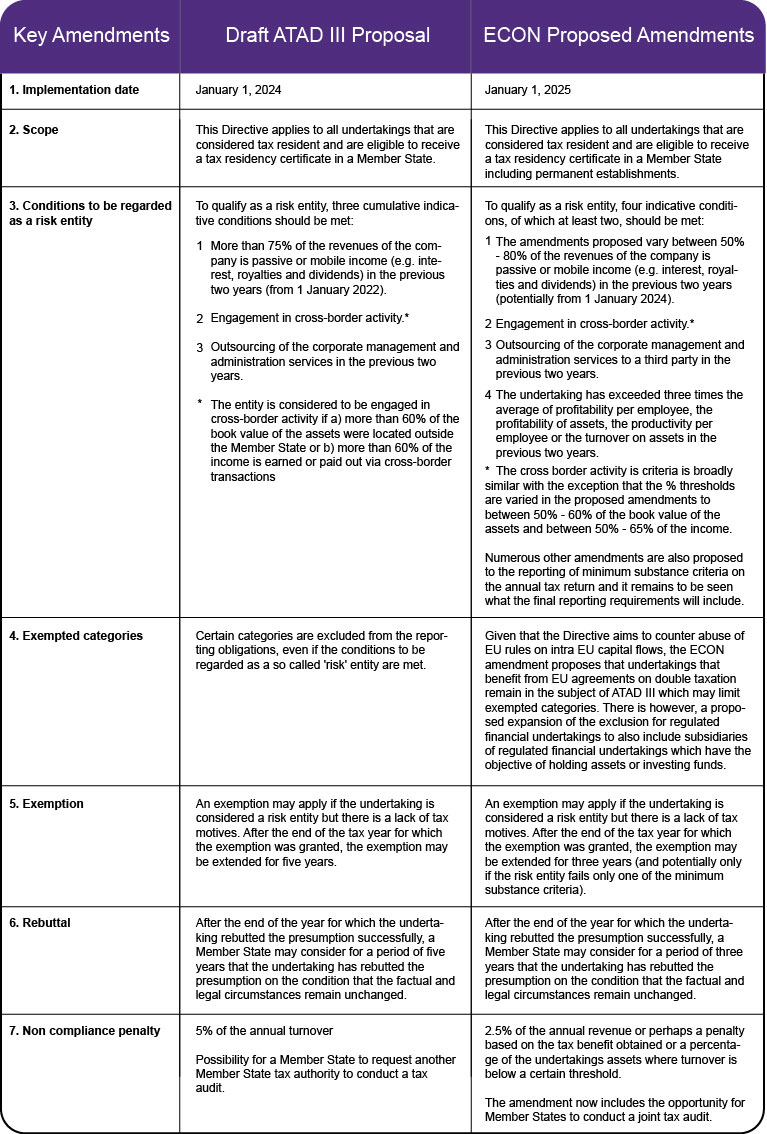

The European Parliament’s Committee on Economic and Monetary Affairs (“ECON”) first issued a number of proposed draft amendments to ATAD III in May. Further draft amendments were published in September. The following table highlights the key proposed amendments.

Current status of ATAD III

In a positive development, and acknowledging the challenge for taxpayers in preparing for the Directive, the ECON has proposed an extension to the timeline for implementation. This would see the new legislation apply from a later date of 1 January 2025 instead of 1 January 2024 and that the two-year periods referred to in the conditions to be qualified as a risk entity will start from 1 January 2023 (or possibly later).

The amendments vary considerably and are not yet definite. It is expected that ECON will vote on 17 November 2022 with a subsequent vote to follow in the European Parliament. The European Commission can accept but also reject the amendments.

How can we help?

Given the proposed implementation dates, we recommend that entities begin assessing their current corporate structures to understand the potential consequences of ATAD III.

Grant Thornton’s international tax specialists can collaborate with you to review your company’s/companies’ current situation with regard to substance and possible exemptions, provide you with the latest information and insights on the detail in the Directive, and offer sensible guidance to be ready if the proposed Directive is passed and implemented.